B2B Crowdfunding Market Overview

No time to read? Let AI give you a quick summary of this article.

The “crowd” of investors has become more diverse. Not only retail backers but also institutions are joining the game. P2P lending and crowd investing have caught the eye of “smart money1”.

It marks two large directions of the crowdfunding market development: consumer fundraising and business crowdfunding. Herein, we’re discussing the evolution of the fundraising industry, B2B crowdfunding trends and the role of institutions in business financing. Let’s go.

What you will learn in this post:

4 waves of modern crowdfunding market development

The global financial crisis in 2008, stricter capital adequacy and solvency requirements for credit institutions, and the explosion of internet usage and usability gave a boost to alternative financing that appeared in the early 2000s.

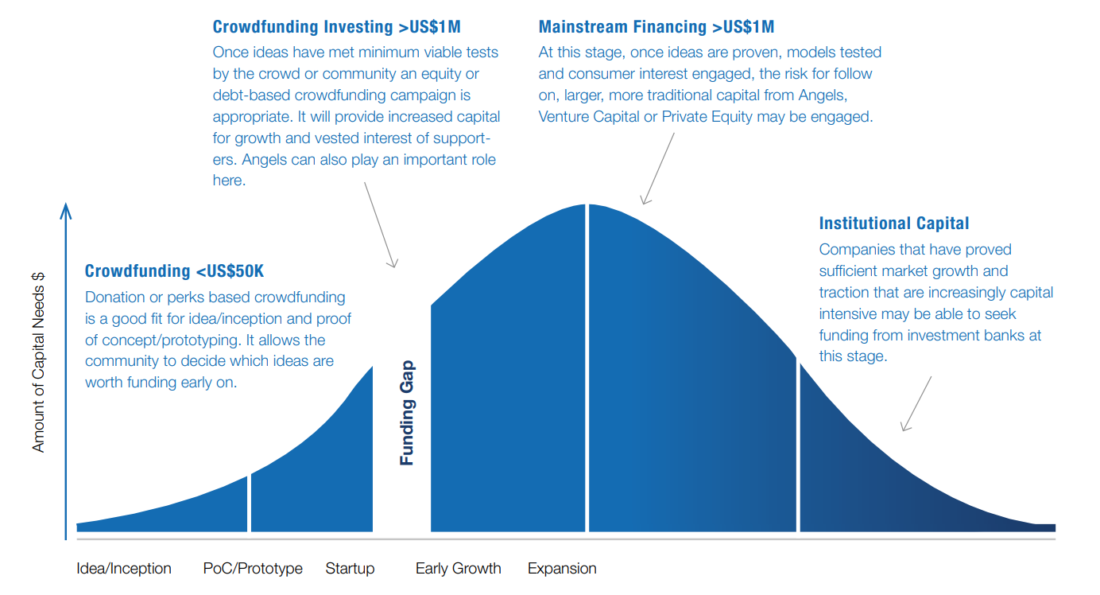

The idea was to simplify fundraising as much as possible by the means of modern technology, from a few months needed in the past to get money to a few days/weeks.

2008-2012

Indiegogo, Kickstarter, Crowdcube, and Seedrs appeared on the landscape.

2012 was a breaking year. The JOBS act “the crowdfunding bill” was adopted in the USA. It put crowdfunding under a legal umbrella for the first time.

The UK authorities launched the 1st consultation paper2 – the new approach to crowdfunding in 2013.

European SMEs resorted to alternative financing when the European Securities and Markets Authority issued its opinion on investment-based crowdfunding3. Professional investors are joining the gam4e and B2B equity crowdfunding is steadily growing.

2012 – 2016

Heavy marketing of alternative finance was paired with the lack of industry knowledge, tons of regulatory speculations5, researches and discussions6.

2017 – 2020

New restrictions and updates (the FCA bans the marketing of mini-bonds7), as a result, some platforms like Crowdlords 8were blocked and banned. The demand for advanced functionality of platforms gave birth to crowdfunding software providers and developers like LenderKit. Institutions demonstrate a growing interest in crowd investing and p2p loans.

2021-2022

The industry is booming again, in particular, due to the COVID-199. New speculations on crypto crowdfunding, blockchain10 and asset tokenization take place. It’s spurred by the SEC increasing crowdfunding limits, match-funding practices in Europe11, new crowdfunding regulation frameworks12 and markets13.

Governments and international institutions globally are actively forcing the cooperation between public and private actors in order to boost sustainable development.

The role of institutions in crowdfunding

Just to clarify, currently, there’s no official term for B2B crowdfunding since all fundraising models suppose that both individuals and institutions play the game.

Therefore you’ll hardly find dedicated B2B crowdfunding websites, all sites are for retail backers and institutions. You can use our CrowdSpace directory for researching crowdfunding platforms in Europe.

The University of Cambridge distinguishes14 business loans as a part of p2p/marketplace lending. Individuals and/or institutional funders provide a loan to a business borrower.

Within investment-based models, institutions can purchase equities issued by the company (equity-based crowdfunding) or securities such as shares, and shares in the profits or royalties of the business (profit sharing).

Also, there’s balance sheet business lending when the platform entity provides loans directly to the business owner.

As VBDO states in its white paper15, that institutions tend to donate money to platforms rather than directly to projects.

The problem is that projects are often too small and the risk-return rate is unclear and uncertain.

The right match? Whitepaper

P2B and B2B crowdfunding market overview

The University of Cambridge presented some good stats16 on P2P business loans and balance sheet business crowdfunding. Here are some facts about the P2B crowdfunding market:

- The largest part of institutional funding is based on crowdlending models. For the past two years, the volumes of institutional funding in P2P/Marketplace and balance sheet business lending have grown and reached $13 billion and $21.2 billion in 2020, respectively.

- China is still among the crowdfunding leaders. However, in 2019-2020 the local alternative finance system experienced a decline. The volumes of business loans dropped by 59% in 2019 ($21 billion) and declined further by 26% ($15 billion) in 2020.

- Firms are shifting to balance sheet activities supported by institutional investors to get seed capital.

- Currently, debt-based models are demonstrating a greater market concentration.

- In terms of risks, p2p loans are believed to be more certain than consumer loans. Balance sheet business lending, on the contrary, delivers higher risks than the consumer model.

- Real estate and property fundraising are booming as an effect of advances in equity-based models. However, the COVID-19 pandemic slowed down crowd investing.

- In terms of global volumes, crowdfunding accounted for $4 billion in 2019 and $4.4 billion in 2020.

- International crowdfunding makes up only 10% of the entire market.

So, as far as we can see, debt-based business models are more preferred among investors compared to crowd investing models. Lending schemes are less risky than consumer loans. Balance sheet business lending is gaining momentum with institutional investors greatly contributing to this mainstream.

Opportunities for institutional investors in B2B crowdfunding business

Despite the fact that crowdfunding projects are often small-scale and indefinite for institutions, they may create another opportunity – impact investing.

Today the global community of investors are seeking sustainable projects to splurge. Although the lack of scale and track records can scare potential investors, sustainable projects deliver a lot of benefits for institutions:

- Institutions can create a direct positive impact and foster the accomplishment of global SDGs and national objectives.

- A status of impact investor helps organisations and institutions generate public trust and create a positive image.

- Crowd financing has different shapes and offers lucrative opportunities for professional angels in terms of profit/risk ratio.

- The alternative finance market is developing at a breakneck speed: a demand creates new niches like fundraising for legal actions, green crowdfunding, shariah-compliant investing, etc.

VBDO suggests15 how bodies and governments can engage institutions in crowdfunding:

- Deeply study the demand, needs and requirements of institutions for B2B fundraising;

- Governmental guarantees may decrease the risks of alternative financing for professional angels;

- Platforms may offer hybrid opportunities when institutions combine crowdfunding deals with venture investments;

- Regulatory sandboxes will simplify the collaboration between platforms and backers in the pilot mode.

Looking for a ready-made solution or exloring a custom build?

Here's how we can help

Summary

Crowdfunding is no longer the prerogative of individual accredited investors and retail backers, institutions tempted by appealing opportunities are entering the industry.

For now, B2B fundraising is a subdomain of p2p lending and crowdinvesting. Alongside individuals, institutions support projects of different kinds: property, green energy, legal actions, education.

Sustainable investing seems to be very appealing for professional backers as it lets them take part in the sustainable development mainstream and create a positive public image.

Given that crowdfunding worldwide remains a risky industry for “smart money”, regulatory bodies and governments should take action to solve the situation. Hybrid deals, governmental guarantees and regulatory sandboxes can force institutions to donate more.

If you’d like to pursue a crowdfunding business idea and set up an online crowdfunding platform, consider using LenderKit – a white-label crowdfunding software platform for B2B and B2C investment businesses.

Article sources:

- PDF (https://www.spglobal.com/marketintelligence/en/documents/an-iq-test-for-the-s...)

- CP13/13: The FCA’s regulatory approach to crowdfunding (and similar activities) | FCA

- Opinion - Investment-based crowdfunding

- Professional investors join the crowdfunding party

- SEC Rules 506(B) And 506(C): Clearing Up The Confusion - Crowdfunding & FinTech Law Blog

- Press - Crowdfunding & FinTech Law Blog

- FCA confirms speculative mini-bond mass-marketing ban | FCA

- Crowdfunding UK, Property Investment London, Crowdfunding Property | CrowdLords

- In particular, due to the COVID-19

- Swapping the underlying technology of crowdfunding contracts for blockchain – the perspective of Roger's five perceived attributes of innovation

- EUROCROWD Report Explains Combining Crowdfunding And European Structural And Investment Funds | Crowdfund Insider

- Just a moment...

- PDF (https://www.fsdafrica.org/wp-content/uploads/2019/08/16-11-07-Crowdfunding_Re...)

- PDF (https://www.jbs.cam.ac.uk/wp-content/uploads/2020/08/2020-04-22-ccaf-global-a...)

- PDF (https://www.vbdo.nl/wp-content/uploads/2019/05/Institutional-investors-crowdf...)

- PDF (https://www.jbs.cam.ac.uk/wp-content/uploads/2021/06/ccaf-2021-06-report-2nd-...)