Democratizing Access to Private Credit via Blockchain

No time to read? Let AI give you a quick summary of this article.

Blockchain is changing the financial landscape and the private lending sector is not an exception. Traditionally, access to private credit markets has been confined to institutional investors and high-net-worth individuals. This used to leave a vast majority of potential investors sidelined.

However, the integration of private credit with blockchain technology, referred to as on-chain private credit, is democratizing this space by expanding investor access, streamlining loan origination, enhancing transparency in risk assessment and repayment tracking.

Here, we will check the nuances of on-chain private credit versus traditional private credit, delve into the mechanics of how it operates, highlight key platforms facilitating this innovation, and examine various use cases that illustrate its impact.

What you will learn in this post:

Traditional private credit vs. on-chain private credit

Private credit involves loans provided by non-bank entities, such as investment funds and specialty finance companies, to businesses or individuals without the intermediation of traditional banks. This sector has grown substantially, managing approximately $1.5 trillion in assets globally1.

Traditional private credit transactions are often characterized by limited transparency, lengthy settlement times, and restricted accessibility. Investors typically rely on intermediaries, and this leads to increased costs and reduced efficiency. The lack of a centralized platform for information sharing can result in asymmetries that affect decision-making processes.

On the other hand, on-chain private credit benefits from blockchain technology to address these challenges2. By bringing private credit transactions onto a decentralized ledger, blockchain enables:

- Transparency: All transactions are recorded on an immutable ledger, which allows participants to verify and audit activities in real-time.

- Efficiency: Smart contracts automate processes such as loan origination, servicing, and repayment. It reduces the need for intermediaries and expedites settlements.

- Liquidity: Tokens can be traded on specialized marketplaces, which enhances the secondary market liquidity3.

- Accessibility: The tokenization of credit assets allows fractional ownership, which enables a broader range of investors to participate in private credit markets.

For example, JPMorgan’s Onyx platform has demonstrated4 the scalability and efficiency of blockchain by processing nearly $700 billion in short-term loan transactions, bypassing traditional systems like SWIFT and enabling nearly instantaneous settlements.

How on-chain private credit works

Here is how the on-chain private credit works.

First, private credit is converted into digital tokens on a blockchain. This process involves creating a digital representation of the asset that can be easily transferred and divided among investors.

All the terms of the agreement between borrower and lender are contained in smart contracts encoded into code. Smart contracts automatically enforce contractual obligations, such as interest payments and principal repayments. This reduces the need for manual intervention.

Finally, blockchain-based platforms provide secondary markets for trading tokenized credit assets. They facilitate the matching of borrowers and lenders and also provide due diligence information.

Platforms that work with on-chain private credit

Several platforms already work with on-chain private credit.

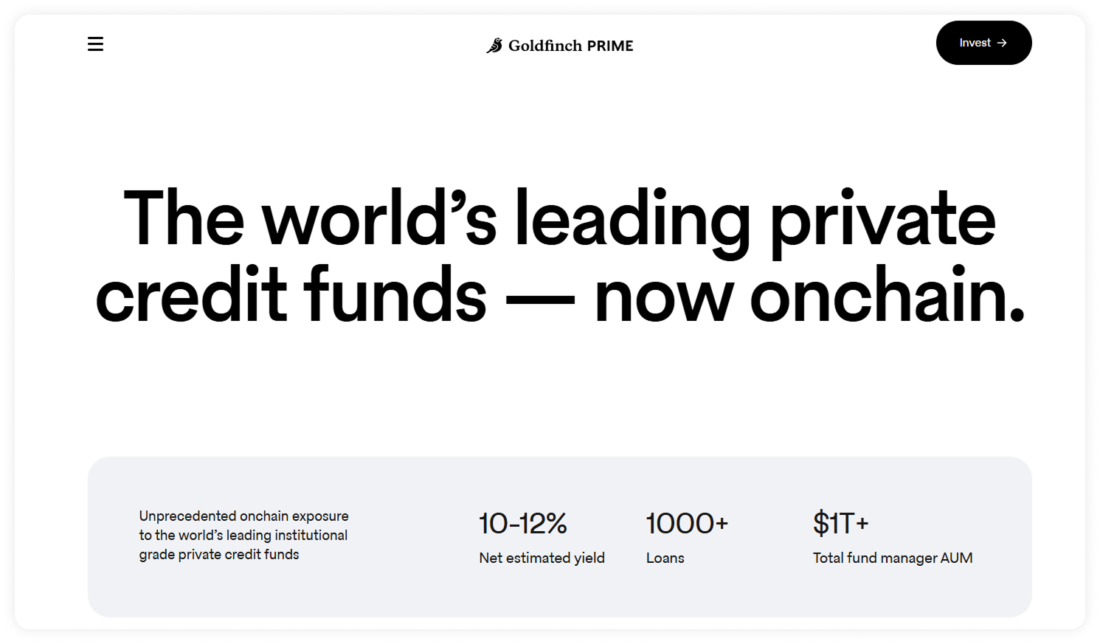

Goldfinch

Established over four years ago, Goldfinch5 aims to bring real-world finance on-chain. Its Goldfinch Prime product offers investors access to multi-billion dollar private credit funds from asset managers like Ares6, Apollo7, and Golub Capital8, all within a single on-chain pool. This composite product streams yield on-chain and provides sustainable returns.

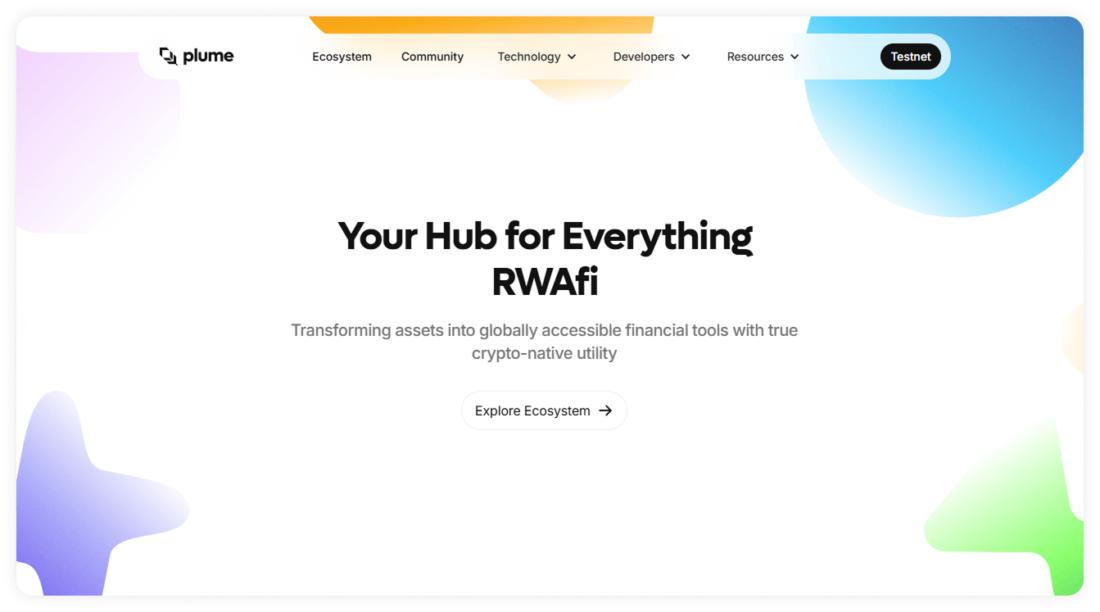

Plume Network

As a modular blockchain tailored for real-world asset finance (RWAfi), Plume9 simplifies the tokenization and integration of real-world assets into the blockchain ecosystem. With over 180 protocols built on its network and a $25 million RWAfi Ecosystem Fund, Plume offers a composable, EVM-compatible environment for managing diverse real-world assets.

Idle

This platform10 has launched on-chain private credit vaults that allow users to lend directly to businesses. By leveraging blockchain technology, Idle aims to provide efficient and transparent lending solutions and connect investors with borrowers in a decentralized manner.

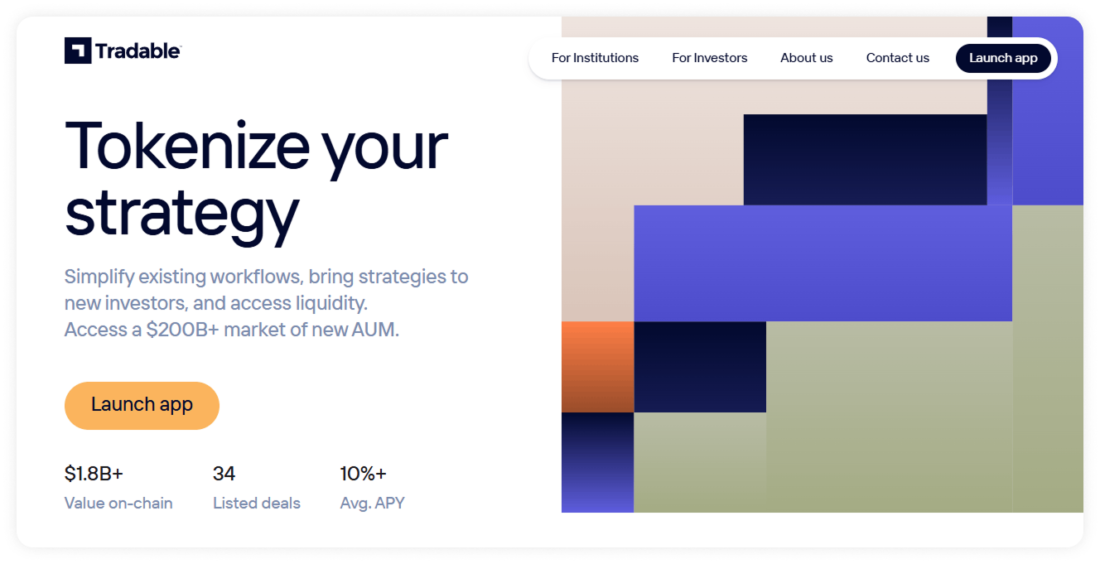

Tradable

Tradable11 is a real-world asset tokenization platform that has tokenized approximately $1.7 billion in private credit on the ZKsync network. Tradable focuses on institutional-grade credit positions. It offers yields between 8% and 15.5%.

Use cases of on-chain private credit

The integration of private credit with blockchain technology has led to several innovative applications.

Fractional ownership for democratization of investment

Fractional ownership democratizes investment opportunities. Expensive assets can be divided into several tokens that represent fractions of the asset. This lowers the entry barrier for investors. This way, retail investors can participate in markets previously reserved for institutional players. Fractional ownership allows the promotion of financial inclusion.

More liquidity to private credit assets

Traditional private credit assets are often illiquid, with lengthy lock-up periods. Tokenization facilitates secondary market trading and provides investors with the option to buy and sell their holdings more readily, thereby enhancing liquidity12.

Streamlined cross-border transactions

Blockchain’s decentralized nature allows for seamless cross-border lending and borrowing. This reduces the complexities and costs associated with international transactions and lowers the transaction costs.

Transparency and security

The immutable nature of blockchain ensures that all transaction data is transparent and tamper-proof. It builds trust among participants and reduces the risk of fraud.

Easier compliance and reporting

Smart contracts can be programmed to enforce compliance with regulatory requirements automatically. This not only simplifies reporting processes but also ensures adherence to legal standards.

Challenges and considerations

While the prospects of on-chain private credit are promising, it faces several challenges that need to be addressed.

Regulatory uncertainty

The regulatory landscape for blockchain-based financial products is still evolving. This is why it is difficult for platforms to ensure full compliance with existing laws and adapt to new regulations rapidly.

Security concerns

Smart contracts and blockchain infrastructure, while robust, are not immune to vulnerabilities. Security audits and risk management strategies must be in place to mitigate potential threats.

Adoption barriers

Traditional financial institutions and investors may be slow to adopt blockchain-based credit solutions due to unfamiliarity, perceived risks, or regulatory concerns.

How to launch a blockchain-based private credit platform with LenderKit

Launching a blockchain-based private credit platform is a multi-step process. At LenderKit, we combine our white-label investment software with tokenization solutions like Polymesh or NYALA to help you reduce the development time and streamline the go-to-market strategy for your business.

Unlike building from scratch, our solutions will accelerate your development, ensure compliance with KYC/AML regulations, and provide a secure environment for lenders and borrowers. To find out how the product works and discuss details, please get in touch with us.

Article sources:

- What Is Private Credit Tokenization and How Does It Work?

- Crypto for Advisors: Private Credit Meets the Blockchain

- Private Credit: The Emerging Trend of 2025 » Particula - The Prime Rating Provider for Digital Assets

- Transforming Private Credit Through Tokenization

- Goldfinch Prime: The world's leading private credit funds onchain

- Ares Management |

- Home | Apollo Global Management

- Golub Capital - Direct Lender and Private Credit Asset Manager

- Plume | The public blockchain for scaling RWAs

- Idle Institutional

- We Make Private Credit Tradable

- Tokenized Private Credit: A New Digital Frontier for Real World Assets | S&P Global