Norway Crowdfunding in 2026: Market, Platforms, Regulations and Software Opportunities

No time to read? Let AI give you a quick summary of this article.

We noticed an intriguing activity spike in our 2020 article about crowdfunding in Norway. So, we asked ourselves why are people suddenly searching for “norge crowdfunding” in 2026?

Has the market started growing? Have new platforms emerged? Are people simply looking for information about companies that no longer exist? Or is it just Google’s algorithm update playing tricks on us?

We decided to dive deeper into the topic to explore how the landscape has evolved, what’s changed on major platforms, and whether there are any new developments in Norwegian crowdfunding in 2026 and beyond.

What you will learn in this post:

What crowdfunding in Norway looked like in 2020

You’re reading that updated article now, but back in the day, Norway’s crowdfunding market reached a major milestone, surpassing NOK 500 million in funding during the first three quarters of 2020, exceeding the entire 2019 annual volume of NOK 442 million1.

Investment-based crowdfunding accounted for 71% of the market, led by P2P property lending (31%) and business lending (27%), with equity crowdfunding making up the remaining share.

Donations and rewards represented approximately 29% of total market activity, highlighting the continued importance of community-driven fundraising alongside investment models. Compared with other Nordic countries, Norway ranked second in donation crowdfunding, while Finland led in equity crowdfunding, Denmark in P2P property lending, and Sweden in balance sheet consumer lending.

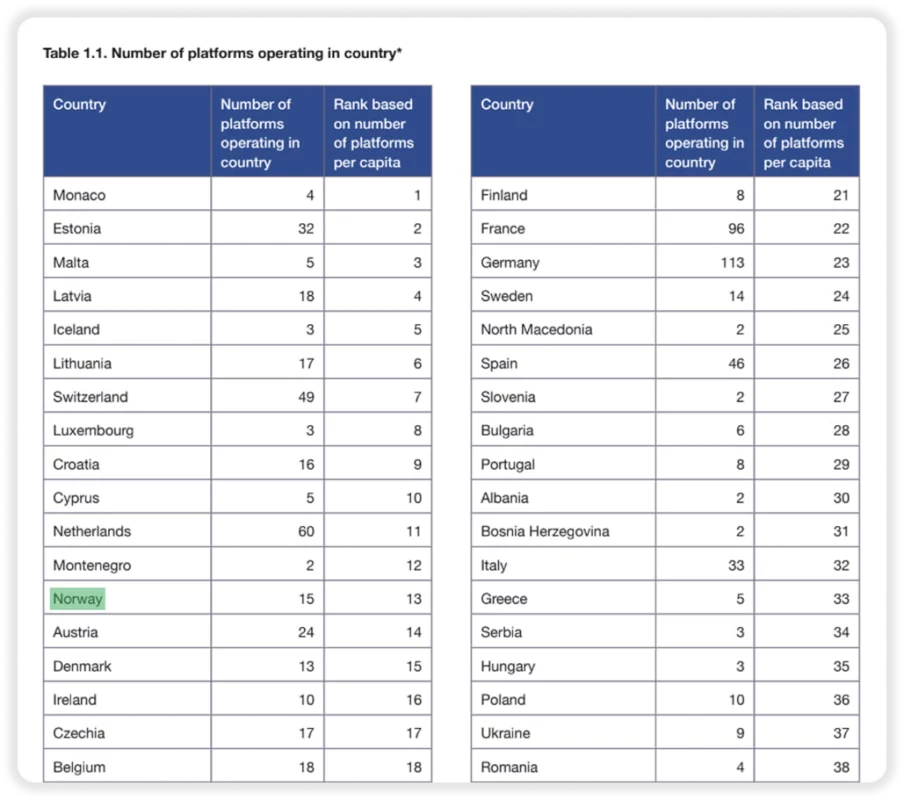

As of 2017-2020, there were 14 locally-based platforms and 7 foreign-based platforms operating in the Norwegian market, including, but not limited to:

- Debt crowdfunding: Monner.no, FundingPartner, Kameo, PERX, and Kredd

- Equity crowdfunding: DealFlow, Folkeinvest, and SparkUp

- Donations and rewards: Bidra, Spleis, and Startskudd

Norwegian crowdfunding market in 2026

Six years on, the answer to our own question is fairly clear: the Norwegian crowdfunding market hasn’t grown so much as it has matured. Around 10-15 platforms are active today, and the ones that remain are more established and specialized.

- Norsk Crowdfunding Forening2 (NCF) merged with Fintech Norway in 2023

- PERX3 bankrupted in 2025

- Monner4 was acquired by Sparebank 1 SR-Bank in 2019

- Lendwill5 shut down and went out of business in 2026

- Kredd6 closed in 2021

- Startskudd7 is no longer active (deadpooled)

- Bidra8 is closed in (deadpooled)

- Folkeinvest9 filed for bankruptcy and is permanently closed, despite claiming to have 60,000 – 70,000 registered investors on the platform.

Source: Crowdfunding industry report 2023

The dynamics definitely hint more towards market consolidation than expansion or growth, but not everything is as grim as it seems.

Crowdfunding platforms in Norway

The Norwegian market has become smaller, but several established platforms continue to operate successfully within clearly defined niches.

- FundingPartner10 focuses on financing Norwegian SMEs and commercial real estate projects, positioning itself as one of the country’s leading business lending platforms.

- Kameo11 has expanded beyond Norway into a broader Nordic presence, specializing in secured real estate lending and demonstrating increasing regional integration across Scandinavian crowdfunding markets.

- Folkeinvest12 remains Norway’s leading equity crowdfunding platform, helping startups and growth companies raise capital through regulated share offerings.

- Oblinor13 continues to specialize in secured real estate lending, while Dealflow14 combines equity crowdfunding with private investment opportunities aimed at growth companies.

Compared with the diverse platform landscape that existed several years ago, today’s market is noticeably more concentrated, with fewer but generally more specialized participants.

Taken together, the market has shifted from a diverse early-stage ecosystem with frequent platform entry and exit to a more concentrated structure dominated by a limited number of established operators.

The Norwegian Crowdfunding Association, which was representing the sector earlier, became part of Fintech Norway15, reflecting how the industry itself has matured.

As crowdfunding became more integrated with the wider financial technology sector, its industry representation evolved from a dedicated crowdfunding association into a broader fintech organization.

Today, crowdfunding sits alongside payments, digital banking, lending, and other fintech verticals within the same industry body.

Crowdfunding market research in Norway

Norway is home to one of Europe’s leading academic research groups dedicated specifically to crowdfunding. The Center for Crowdfunding Research16 at the University of Agder17 has spent years studying crowdfunding markets, investor behavior, regulation, and platform development through both national and international research projects.

One of the leading figures behind this work is Professor Rotem Shneor18, whose research has contributed to numerous European and global crowdfunding reports. His work demonstrates that crowdfunding is no longer simply a fintech trend but an established area of financial research supported by universities, policymakers, and industry participants.

Crowdfunding regulation in Norway

Perhaps the most significant difference between today’s market and the early crowdfunding years is regulation.

Norwegian platforms operate under the supervision of Finanstilsynet19, which oversees financial institutions, investor protection, anti-money laundering (AML) compliance, and Know Your Customer (KYC) requirements.

Although Norway is not an EU member, the country’s participation in the EEA means that European regulatory developments continue to influence the market. Platforms seeking to operate internationally increasingly align their operations with ECSPR20 principles that cover transparency, investor disclosures, governance, and operational standards.

Norway BankID and tech infrastructure

Successful platforms today depend on a much broader technology ecosystem that includes digital identity verification, payment processing, investor onboarding, transaction monitoring, reporting, and portfolio management.

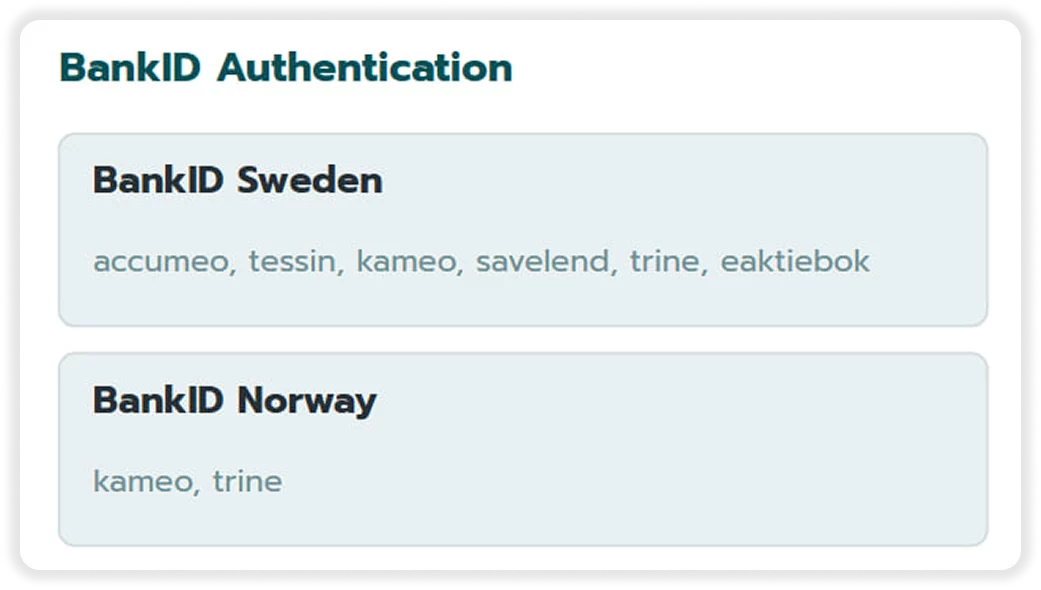

In Norway, digital identity solutions such as BankID21 have become a very important part of the financial infrastructure. It allows platforms to onboard investors securely while meeting strict KYC requirements. Rather than building these capabilities internally, many modern platforms integrate specialized third-party providers for identity verification, payment services, compliance, and financial reporting.

The importance of this infrastructure became particularly visible through cases such as Perx.

While discussions around the platform often focused on its business challenges, they also highlighted how dependent modern crowdfunding businesses are on underlying technology providers, servicing systems, and financial infrastructure. Crowdfunding platforms are no longer simple marketplaces connecting investors and borrowers but they are complex financial technology businesses.

Looking for a ready-made solution or exloring a custom build?

Here's how we can help

Crowdfunding software for launching a platform in Norway

Launching a crowdfunding platform in Norway is more demanding than it used to be. Today, businesses need more than a good idea. They must comply with financial regulations, implement AML and KYC procedures, integrate secure payment systems, and build a reliable platform for investors and borrowers.

Building all of this from scratch takes time, money, and technical expertise. In many cases, development can take months or even years before the platform is ready to launch.

That is why many businesses choose a white-label crowdfunding solution instead.

LenderKit is a white-label crowdfunding software provider that helps businesses launch lending and investment platforms faster. Instead of building everything from the ground up, companies receive a ready-made platform that can be customized to match their brand and business model.

LenderKit supports a wide range of crowdfunding models, including:

- Business lending

- Real estate crowdfunding

- Equity crowdfunding

- Peer-to-peer (P2P) lending

- Invoice financing

The platform also includes the tools needed to run a modern crowdfunding business, such as:

- Investor and borrower onboarding;

- KYC and AML integrations;

- Campaign and investment management;

- Payment processing;

- Investor dashboards and reporting;

- API integrations with third-party services.

For businesses planning to enter the Norwegian crowdfunding market, a white-label crowdfunding software like LenderKit offers a faster, more cost-effective path to launch while providing the flexibility to scale in the future.

To find out how the solution works or discuss details, please get in touch with us.

Article sources:

- PDF (https://60563ffc-6f19-46bb-a329-21761c7a12b5.filesusr.com/ugd/390e49_f5b4c670...)

- LinkedIn Login, Sign in | LinkedIn

- Perx Folkefinans

- Monner was acquired by Sparebank 1 SR-Bank - Nordic9.com

- Https://match.adsrvr.org/track/cmf/rubicon

- Folkefinansieringsselskap avvikler: – Umulig å konkurrere – E24

- Startskudd - 2026 Company Profile, Team & Competitors - Tracxn

- Bidra.no - 2026 Company Profile, Team & Competitors - Tracxn

- The End for Folkeinvest | Finansavisen

- Lån, hils på investering - FundingPartner

- 403 Forbidden

- Folkeinvest

- Oblinor | Innovativ Eiendomsfinansiering for Bærekraftig Vekst

- Dealflow - kapitalkilde for vekstselskaper, investeringsmuligheter for alle

- Home - Fintech Norway

- Concluded Projects | CFRC

- Front page - University of Agder

- Sign Up | LinkedIn

- Home - Finanstilsynet.no

- Regulation - 2020/1503 - EN - EUR-Lex

- BankID