Tokenized Bonds in Practice: What Canada’s Project Samara Reveals About the Future of Digital Securities

No time to read? Let AI give you a quick summary of this article.

Tokenization is becoming a major focus in financial infrastructure. Banks, regulators, and technology firms see distributed ledger technology (DLT) as a practical way to modernize capital markets. Until recently, however, most work on tokenized securities stayed theoretical or limited to small pilot projects.

Canada’s Project Samara1 changes that.

Led by the Bank of Canada2, in collaboration with Export Development Canada (EDC)3, Royal Bank of Canada4, and TD Bank Group5, the initiative tested whether a bond could be issued, traded, and settled entirely on distributed ledger infrastructure.

The result was Canada’s first tokenized bond6: a CAD 100 million short-term security issued on blockchain-based infrastructure.

In the article, we will check the main outcomes of Project Samara, and why it may change the future of digital securities.

Also read: Self-Certified Investors in Canada: What It Means for Crowdfunding and How to QualifyWhat you will learn in this post:

How the bond issuance process works: Traditional model vs DLT

One of the most useful parts of the project is a simple comparison between traditional bond issuance and the DLT-based approach.

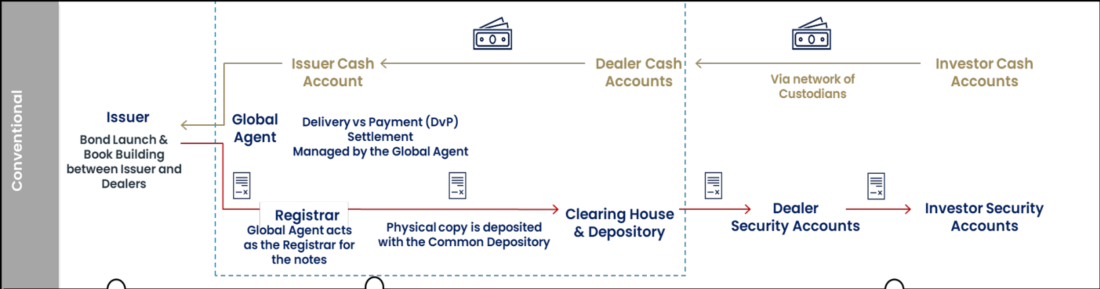

Traditional bond issuance

In a traditional bond issuance, the process follows a clear but multi-step sequence.

The issuer appoints dealers: The issuer selects one or more dealers (underwriters) to structure the deal and place the bond with investors.

The deal is prepared: At this stage, the issuer and dealers define the size of the bond, its maturity, the interest rate, and the expected price range. At the same time, legal teams begin preparing the required documentation.

Marketing to investors begins: Dealers reach out to institutional investors and present the offering. This stage is often called bookbuilding.

Investors submit orders: Interested investors indicate how much they want to buy and at what price or yield. Dealers collect those orders into a single order book.

Allocation is decided: Based on demand, the issuer and dealers set the final price and decide how much each investor receives.

Legal documentation is finalized: All agreements are completed and signed.

The bond is created and registered: The bond is formally issued, a registrar records ownership details, and a fiscal or paying agent is assigned to manage payments.

Securities are sent to the securities depository, which acts as the main record-keeper for ownership.

Custodians update investor accounts: Each investor’s custodian updates internal systems to reflect the new holdings.

Cash is transferred: Investors send payment through the banking system.

Settlement is completed: The bond is delivered to investors, and payment is received by the issuer.

Each stage of the process is handled by a different party, and their systems are not connected. As a result, the same data has to be recorded multiple times, and information moves back and forth between institutions.

Nothing is finalized until the very end, when settlement finally takes place.

Because of this structure, the full process usually takes three to five business days (T+3 to T+5). It is a well-established system, but it depends heavily on coordination between participants rather than automation.

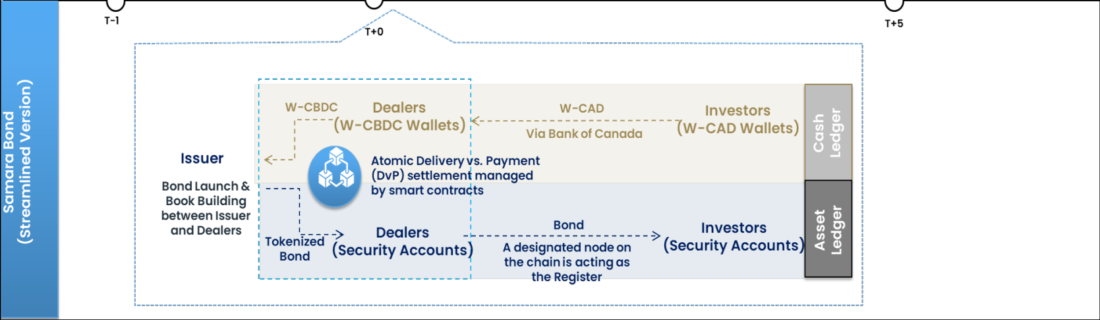

Samara model bond issuance

At the center of the experiment was the Samara Platform, a system built specifically to test how tokenized bonds can work in practice.

It runs on Hyperledger Fabric7, a type of blockchain designed for financial institutions. Unlike public blockchains, access is restricted, so only approved participants can join and operate within the system.

The platform is built around two connected parts:

- Asset ledger records the bond as a digital (tokenized) asset

- Cash ledger holds digital cash, known as wholesale Canadian dollars (W-CAD)

These two ledgers work together as one system. Bond issuance is handled as a single, coordinated process on a distributed ledger.

First, the issuer defines the bond terms, just as in a traditional setup. The difference is that the bond is created directly as a tokenized asset on the platform. At the same time, investors prepare funds in W-CAD, which is digital wholesale central bank money used for settlement on the system.

Next, investors submit their interest, similar to bookbuilding, but this happens within the platform environment. Orders are collected, and allocations are determined. Once allocations are set, the bond is issued on the ledger.

This is where the process changes completely.

Instead of moving through multiple intermediaries, the platform handles everything. Smart contracts coordinate the transaction, and an interledger mechanism links the asset and cash ledgers.

Then, atomic delivery-versus-payment (DvP) takes place. The bond is delivered to investors, and payment is made at the same time. In simple terms, either both sides of the deal go through, or nothing happens at all. This removes the risk of one party paying while the other fails to deliver.

Issuing Canada’s first tokenized bond

At the center of the experiment was a real bond.

Export Development Canada issued a CAD 100 million bond with a maturity of less than three months. It was offered to a select group of institutional investors.

What made this bond different was not its size or structure, but how it was handled. Instead of using traditional financial infrastructure, the bond was created as a tokenized asset on the Samara platform. It existed directly on the distributed ledger.

Settlement was done using wholesale central bank money provided by the Bank of Canada. The setup was designed to reflect real market conditions as closely as possible. This means the project did not just test tokenization in isolation. It tested how a digital bond actually works from start to finish in a real financial setting.

Why bonds are a natural starting point

Bonds are a good starting point for tokenization because they follow clear, predictable rules. They have fixed processes, such as regular coupon payments and repayment at maturity. These steps are easy to automate using digital assets.

At the same time, bond markets still face several well-known issues:

- slow settlement

- fragmented records across institutions

- constant need for reconciliation

Tokenization helps address these problems by placing both the bond and the payment on a single system. This simplifies the process and reduces the need for intermediaries.

Operational improvements

One of the most important goals of the experiment was to evaluate whether DLT could improve operational efficiency. And indeed, there were some important improvements:

- Faster settlement: Transactions settle almost instantly on the platform. It helps to reduce delays and counterparty risk.

- Simpler workflows: All participants use the same system, so there is no need to reconcile separate records.

- Better transparency: Data is shared in real time, this is why transactions are easier to track and verify.

Challenges

Despite the technical success of the pilot, Project Samara also highlighted several challenges.

- Integration with existing systems: Connecting DLT to legacy infrastructure is complex and expensive.

- Liquidity and adoption: The system needs enough participants to work efficiently; otherwise, liquidity may be limited.

- Regulatory uncertainty: Questions remain around legal status, custody, and settlement rules for tokenized assets.

What this means for digital securities

Project Samara shows that tokenized bonds already work in a real market setup. A distributed ledger can support issuance, trading, and settlement within a single system.

But it also makes one thing clear: change will be gradual.

Adoption depends on:

- regulation

- market participation

- integration with existing infrastructure

The most likely outcome is a hybrid model, where traditional systems and digital platforms operate side by side.

How to build an investment platform with LenderKit

If this shift continues, the next step is not just issuing digital securities but making them accessible. This is where investment platforms come in. Building such a platform from scratch is complex. It requires handling investor flows, asset management, and transaction tracking, all within a regulated environment. This is where white-label investment software solutions, such as those offered by LenderKit, make a difference.

LenderKit provides the essential tools to launch an investment platform which includes:

- investor onboarding and management

- deal creation and asset listing

- transaction tracking and reporting

Instead of building everything yourself, you can rely on a ready system designed for real-world use. This allows you to launch faster, operate more efficiently, and adapt as digital securities become a standard part of financial markets.

To see how LenderKit’s white-label solutions can work for you or discuss details, please get in touch with our team.

Article sources:

- PDF (https://www.bankofcanada.ca/wp-content/uploads/2026/03/sap2026-8.pdf)

- Bank of Canada pilot issues country’s first tokenized bond — TradingView News

- Export Development Canada (EDC)

- Welcome to RBC Personal Banking - RBC Royal Bank

- Online Banking, Loans, Credit Cards & Home Lending | TD Bank

- Bank of Canada, Export Development Canada, RBC and TD successfully complete bond issuance experiment using distributed ledger technology - Bank of Canada

- A Blockchain Platform for the Enterprise — Hyperledger Fabric Docs main documentation