How P2P Lending Platforms Become Banks: Real-World Case Studies

No time to read? Let AI give you a quick summary of this article.

Peer-to-peer lending began with a simple idea: use technology to unbundle traditional banking and connect borrowers directly with investors. The model proved itself. Platforms scaled, credit performance improved, and millions of customers adopted marketplace lending as a viable alternative to banks.

Over time, three P2P lending platforms — Mintos, Zopa and Fellow Finance — reached a new inflection point.

Having built strong risk capabilities, trusted brands, and sustainable economics, they began to look beyond pure intermediation.

For these platforms, becoming a bank was not a rejection of the P2P model, but its logical evolution — a way to extend what worked into a broader, more resilient financial institution.

Below are three real-world examples of how that transition unfolds in practice.

What you will learn in this post:

1. Mintos: From a marketplace to bank ambitions

Mintos is one of Europe’s largest P2P investment marketplaces, founded in 2015 and headquartered in Riga, Latvia. It built scale fast by letting investors fund loans originated by third parties across multiple countries and loan types. Over time, it broadened its services to fractional bonds, ETFs, and even real estate investments.

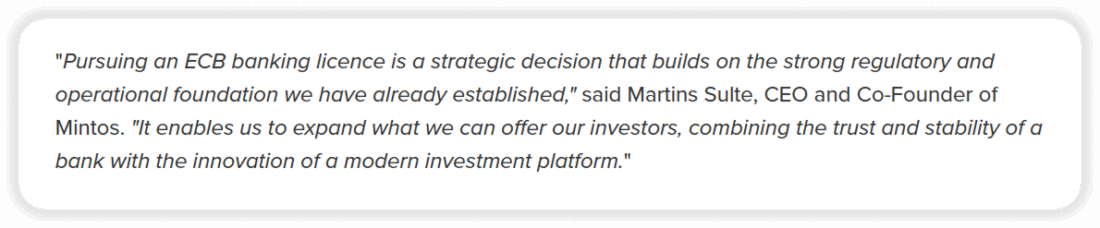

In early 2026, Mintos officially began the regulatory process1 to secure a full banking licence from the European Central Bank (ECB)2.

Why pursue a banking licence?

P2P platforms generally operate under investment-firm or crowdfunding licences issued by national regulators. That works at a smaller scale, but it limits what they can do:

- They cannot take deposits directly from customers.

- They must rely on third-party banks for core infrastructure like custody, payments, and settlement.

- Investor protection is typically limited to investment-firm rules, not banking-level safeguards.

That is changing.

Getting the licence from the ECB would give Mintos the following benefits3:

- Access to deposit-based funding, which is a much cheaper and more stable source of capital than selling notes to investors.

- Eligibility for EU deposit protection schemes (protecting customer deposits up to €100,000 per person).

- Control over key infrastructure functions, such as custody and settlement, that are otherwise outsourced.

- A broader range of lending and banking products will become available to customers directly.

Scale matters

Mintos now boasts roughly 700,000 registered investors and manages around €800 million in assets, including multi-asset portfolios. Without a bank licence, Mintos simply hosts investment products. With a license, it could integrate deposits, savings, lending, and investment under one regulated roof.

Regulators expect rigorous capital buffers, governance standards, and risk controls before issuing banking licences, and the entire process in the EU can take 12-18 months4 or more. This is complex and costly, but it shows a commitment to long-term viability and customer protection that marketplace licences cannot match.

2. Zopa: From first P2P lender to full UK bank

Zopa has the longest pedigree of any player on this list. The platform was founded in London in 2005 as the first true peer-to-peer lender.

For nearly two decades, Zopa’s marketplace connected lenders and borrowers directly, and by the mid-2010s, it had lent out billions of pounds5.

The bank licence journey

In 2018, Zopa was granted a banking licence6 by the UK’s Financial Conduct Authority (FCA)7 and Prudential Regulation Authority (PRA)8. At that time, its banking licence was in “mobilization”. It means that the company had received formal approval but was working to meet conditions before launching full products.

By 2020, Zopa Bank Ltd. was fully operational9 with regulated products, including:

- FSCS-protected savings accounts

- Credit cards

- Personal loans

- A mobile banking app

These products were offered in parallel with the platform’s marketplace for a time.

Closing the P2P business

By the end of 2021, Zopa made the decision to wind down its P2P marketplace10 completely. The bank arm bought the outstanding P2P loan portfolio and returned capital to investors at full value. This ended the marketplace model after 16 years.

Why?

Several factors played in:

- Regulatory pressure: Authorities tightened rules on risk disclosures, default handling, and investor protections. This made P2P less commercially viable.

- Investor sentiment: A number of platform failures in the sector eroded trust in P2P.

- Stable funding: Bank deposit funding is cheaper and more predictable than relying on marketplace note sales or third-party funding.

- Product breadth: As a bank, Zopa could package savings, payments, and lending in one regulated app with deposit protection. This couldn’t be done within a P2P lending model.

Today, Zopa Bank manages billions in client deposits and loans. This shows that the way from a fintech experiment to a regulated banking provider was a success.

3. Fellow Finance and Alisa Bank: Merger as a route to becoming a bank

Not all platforms apply for a license to become a bank. Some do it through partnerships and mergers.

In Finland, leading P2P lender Fellow Finance Plc has selected exactly this route: they merged with an existing banking institution, Evli Bank Plc11.

On 14 July 2021, the two companies agreed to a combination plan under which Evli Bank would partially demerge into a new asset management group, and its banking service entity would merge with Fellow Finance.

The merger was completed and registered with Finnish authorities in April 2022.

But why did the platform choose a merger instead of applying for a license? Here are some reasons.

- Faster access to regulated infrastructure: Rather than building a bank licence from scratch, Fellow Finance gained immediate access to an existing bank’s licence and infrastructure.

- Enhanced scale and expertise: Fellow Finance brought digital lending and customer acquisition experience, while Evli contributed traditional banking operations and risk management.

This way, the new entity, initially called Fellow Bank and later rebranded as Alisa Bank12, could offer broad financial products to individuals and small businesses, including deposit accounts and loan products.

Why do P2P platforms become banks?

For a small number of mature platforms, the marketplace model eventually becomes a constraint rather than an advantage.

After years of operating at scale, these platforms have already built the core capabilities of a bank: credit underwriting, risk management, customer servicing, and compliance. At that point, obtaining a banking licence is less a reinvention and more a formalisation of what already exists.

Timing matters.

Platforms that make this transition typically do so from a position of strength — with established brands, loyal customer bases, and sufficient capital to absorb the regulatory and operational demands of banking.

A licence unlocks strategic flexibility: access to deposits as a stable funding source, the ability to offer a broader range of products, and greater control over the full financial stack.

In this sense, becoming a bank is not a response to external pressure, but an evolutionary step. It allows successful P2P platforms to move beyond the limits of pure intermediation and operate with the resilience, credibility, and scope required for long-term scale.

How to start your own P2P lending platform with LenderKit

The history of P2P lending platforms turning into banks shows that easy entry is no longer enough. Launching a P2P investment platform involves careful regulatory planning, solid risk frameworks, and scalable technology.

LenderKit can help entrepreneurs build a compliant, modular P2P lending and investment platform without developing everything from scratch.

With LenderKit, you get:

- Debt crowdfunding and p2p lending features

- Investor dashboards and analytics

- Automated payment flows

- Risk scoring and compliance controls

- Investor onboarding and deal management

- API integrations and more

Instead of spending years building, testing, and debugging a P2P lending platform created from scratch, platform owners can use LenderKit and focus on growth.

In a sector where a marketplace can eventually evolve into a fully regulated bank, it’s wise to start with robust technology and compliance baked in. Doing so increases the likelihood of long-term success, whether the platform remains a marketplace or becomes a licensed financial institution.

To discuss details, please get in touch with us.

Article sources:

- European Investment Platform Mintos Aims To Establish A Bank | Crowdfund Insider

- European Central Bank

- Mintos pursues ECB banking licence

- What is the timeline for the banking licence?

- Zopa digital bank to launch in 2019 after FCA grants banking licence

- We’ve received our banking licence – what happens next?

- Financial Conduct Authority | FCA

- What is the Prudential Regulation Authority (PRA)? | Bank of England

- Our story

- Zopa officially exits P2P lending - Alternative Credit Investor

- Fellow Finance and Evli Bank to complete their merger - Alisa Pankki Oyj

- Alisa Bank | Digital Finnish Bank