Reg A vs Reg D vs Reg CF what’s the difference

No time to read? Let AI give you a quick summary of this article.

The USA crowdfunding market is ranked first regionally and second globally, mainly thanks to adequate up-to-date regulation provided by the SEC. According to the Cambridge report1, more than 70% of players consider the current legislative framework appropriate for their investment platform activities.

And it’s a great indicator compared to other countries.

The SEC keeps simplifying and harmonizing the set of rules to benefit every party – platforms, fundraisers and investors.

For instance, on November 2, 2020 the body introduced rule amendments to Reg A, Reg D, and Reg FC offerings2.

These changes are to make guidelines more rational and less complex.

If it’s the first time you hear the regulation alphabet, or you need more clarity to this question, you can check out the best crowdfunding lawyers in the US or read about the difference Reg A vs Reg D vs Reg CF in this quick overview.

What you will learn in this post:

Reg A and Reg D: how the SEC regulates exempt offerings

US and non-US-based companies can offer and sell securities under Reg A3 and Reg D4. Both sets of rules are exemptions of the “Securities Act”.

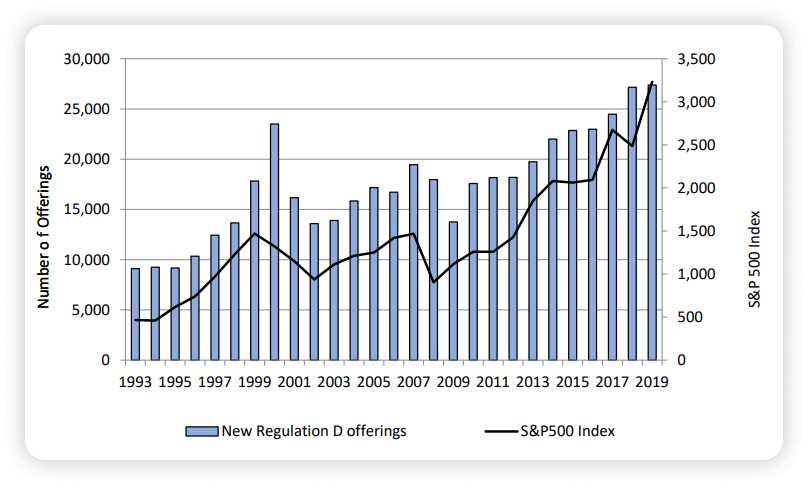

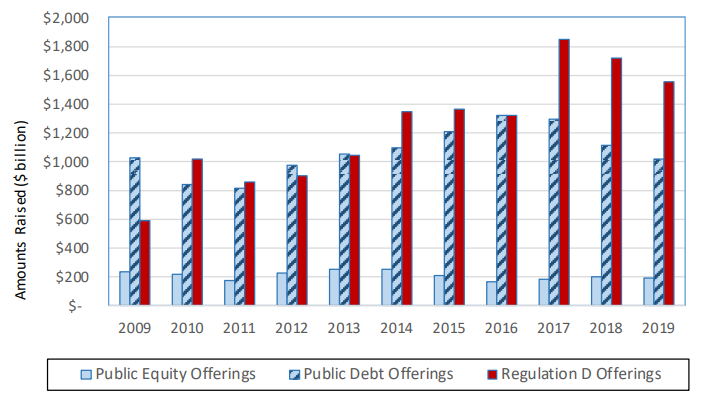

Reg D offerings have always been more popular among fundraisers.

The SEC reports about a steady growth of Reg D offerings5 during the past years. This model accounts for a larger offering market share.

For example, in 2019, under Reg A, there was only $1 billion raised while Reg D offerings amounted for +$1.5 trillion.

What should you know about exempt securities offerings regulation?

Reg A (Reg A+) consists of two tiers (Tier 1 and Tier 2) allowing companies to conduct “Mini-IPOs” distinguished by the upper limit of offerings:

- Reg A Tier 1 enables businesses to collect up to $20 million in a 12-month period;

- Reg A Tier 2 – up to $75 million in a 12-month period.

At rest, companies may comply with standards established for this type of offerings – issuer, investor and SEC filing requirements, disclosure, restrictions of resale, etc.

Due to new rules, general solicitation for Reg A is to be replaced with “Demo Days” and similar events soon.

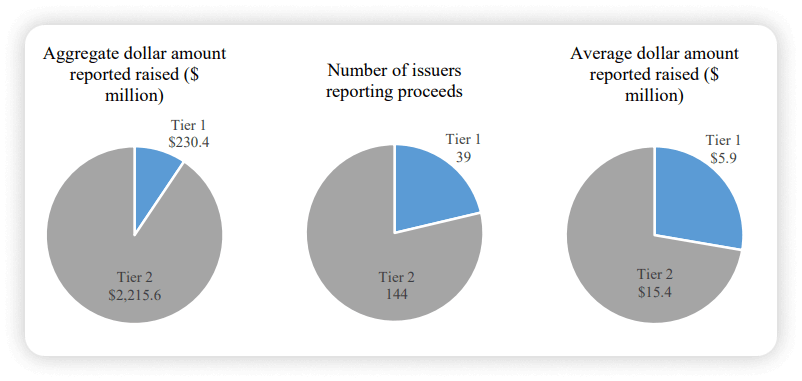

70% of all Reg A-based offerings are registered under Tier 2.

The SEC has analysed all issuers in qualified Regulation A offerings and concluded that the majority of them are small (based on assets and revenues) and relatively young.

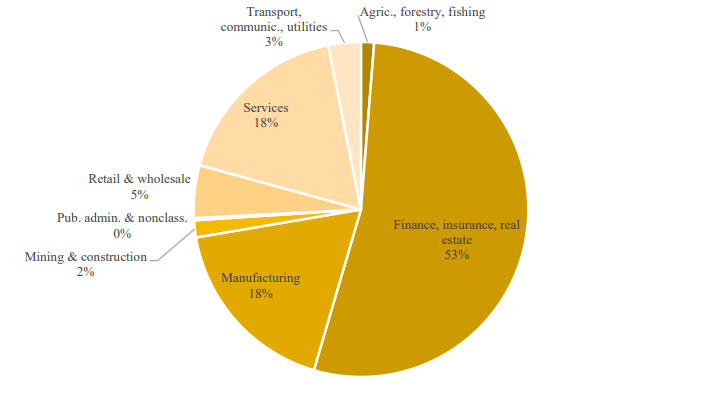

93% of offerings were equity-based and 80% of them were conducted on a continuous basis.

The largest part of offerings (53%) is concentrated in the finance, insurance, and real estate sectors.

Often, REITs, holding companies, non-depository credit institutions, and commercial banks act as financial issuers.

As for non-financial issuers, the majority of players provide business services including software.

An estimated timeline6 for Reg A crowdfunding offerings: 2-4 months, max allowed time – 12 months.

Some examples of the Reg A portals are:

- SeedInvest

- WeFunder

- Banq

Now let’s talk about Regulation D or accredited crowdfunding.

The set of exemptions were adopted in 1982 to simplify rules that existed at that time and strengthen investor protection.

Initially, Reg D included three rules: Rule 504, Rule 505, and Rule 506. In 2017 Rule 505 was abolished. The current Reg D framework consists of Rule 504, Rule 506 (b) and 506 (c).

How do the Reg D rules differ from Reg A?

Rule 5047 is for securities offers and sales of up to $10 million in a 12-month period. Reporting companies, investment companies, and certain development-stage companies can’t issue securities under Rule 504. Also, issuers may not use general solicitation or advertising to market the securities.

Rule 506 (b) is a “non-exclusive safe harbour” enabling issuers to offer and sell an unlimited amount of securities.

There are some conditions for issuers to meet:

- offers don’t imply general solicitation or advertising

- only accredited investors take part in deals

- the max number of non-accredited investors – 35

Rule 506 (c) is more loyal to issuers: no limitation on amounts offered, general solicitation and advertising are allowed. Only if backers are accredited.

Reg D offerings market statistics5:

- in 2019, out of all the Reg D offering types almost all the capital was raised under Rule 506 (b)

- almost 40% of Reg D issuers are private funds, real estate – 25.5%, tech – 20%

- most Reg D issuers are located in California or New York

- 9% of all issuers are non-US-based

- most issuers tend to be small-scale with revenue less than $1 million

- the majority of non-fund issuers raise funds through equity

- Reg D offerings are way popular than public equity or debt offerings

An estimated timeline for Reg D offerings: 100 days.

Some examples of the Reg D portals are:

- FundersClub

- AngelList

- CircleUp

Title III of the JOBS Act and retail crowdfunding

Reg CF crowdfunding defines the requirements for offering and selling securities under Section 4(a)(6) added by Title III of the JOBS Act8 to the Securities Act.

Despite COVID-19, during 2019-2020 capital commitments to Reg CF issuers rose by 77.6%9. The number of investors increased too.

Experts believe it happened due to several factors including industry development, investor education, regulatory changes.

Characteristics of the Reg CF:

- the maximum aggregate amount of funds to raise – $5 million in a 12-month perio

- all deals should take place on a registered provider – broker-dealer or Reg CF funding portal

- investment limitations based on an annual income and net worth;

- bad actors’ disqualification

- disclosure of information in filings is required

According to new rules10 which came into effect in March11, the offering limit was increased to $5 million and investment limits for accredited investors have been removed. Also, the SEC extended the existing temporary relief providing an exemption up to 18 months for issuers offering $250k or less of securities and allow the latter to use SPVs to facilitate investing.

The general solicitation will be replaced with “testing the waters”.

Characteristics12 of crowdfunding issuers and offerings:

- in 2019, most offerings (90%) were conducted through Reg CF funding portals;

- a typical fundraiser is small and early-stage with $30k of assets, $4k holdings and no revenue;

- average amount raised13 per offering in 2020: $342k;

- equity deals prevail over debt and SAFE, their share accounts for 48%;

- top industries13: restaurants, diversified media, personal services, etc.

- the majority of offerings are made in California followed by New York, and Texas;

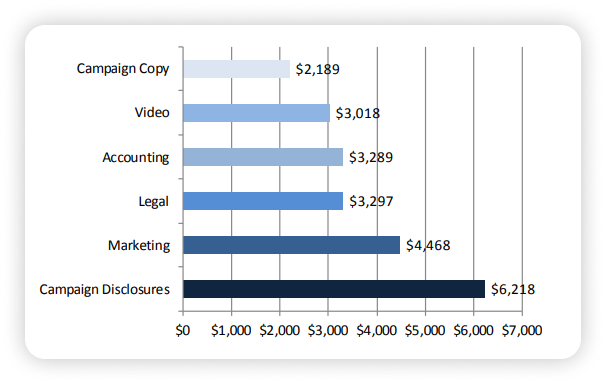

- an average cost of a crowdfunding campaign is 5.3% of the amount raised;

- a median timeline for a crowdfunding campaign under Reg CF – 60-90 days.

Some examples of the Reg CF portals are:

- SeedInvest

- InfraShares

- FlashFunders

- Republic

- WeFunder

Comparing Reg CF vs Reg A and Reg D crowdfunding offerings

There are tons of summary tables on US regulatory frameworks for securities offerings on the web, so we decided not to duplicate this information.

Instead, we’ll summarize how offerings differ by their characteristics. Note, all the numbers are rough estimation of the available data presented in the official reports and open data banks.

| Characteristics | Reg A | Reg D | Reg CF |

| Typical issuer | small and relatively young | small-scale with revenue less than $1m | small and early-stage |

| Mean offer size | $26m | $58m | $208k |

| Top industries | finance, manufacturing, services | private funds, real estate, tech, health care, banking | restaurants, diversified media, personal services |

| Average offering timeline | 2-4 months | 3-4 months | 2-3 months |

| Average offering cost | 12% of the capital raised | 10% to 12% of capital raised | 5.3% of the amount raised |

Looking for a ready-made solution or exloring a custom build?

Here's how we can help

Final thoughts

Regulation is a crucial factor of the finance industry success. Over the past decade regulatory requirements in the US have evolved to keep pace with a rapidly developing complex market of alternative financing.

As crowdfunding providers strive to keep pace with ever-changing regulation, they’re turning to smart solutions assisting them in addressing this issue.

LenderKit is our in-house investment management software developed for US-based crowdfunding businesses.

It helps you launch an equity or debt funding portal or broker-dealer platform under the Reg CF, Reg A or Reg D.

LenderKit software package includes features for automating key capital raising processes and flows – creator and investor onboarding, investment management, transactions and reporting, payment processing via third-party, KYC/AML verification, and more.

LenderKit is suitable for both public and private fundraising and its functionality allows choosing the capital raising method.

In a bundle with LenderKit you get: a marketing website, investor portal, admin back-office which can be customized according to your needs and regulations.

Want to test the feel and look of LenderKit? Schedule a demo.

Please note that this article is for informational purposes only, don’t consider it as legal advice or recommendation. Speak with your lawyer and consult only official resources regarding any up-to-date information on the regulations and policies.

Article sources:

- PDF (https://www.jbs.cam.ac.uk/wp-content/uploads/2020/08/2020-04-22-ccaf-global-a...)

- SEC Harmonizes and Improves “Patchwork” Exempt Offering Framework

- SEC.gov | Regulation A

- Regulation D Offerings | Investor.gov

- PDF (https://www.sec.gov/files/report-congress-regulation-a-d.pdf)

- What Is The Timeline For A Reg A+ Offering?

- Exemption for limited offerings not exceeding $10 million—Rule 504 of Regulation D

- U.S. Securities-based Crowdfunding Under Title III of the JOBS Act

- $239 Million Was Raised Using Reg CF During 2020, This Amount Could Double In 2021 | Crowdfund Insider

- The SEC Adopts Amendments to Regulation Crowdfunding | Kilpatrick - JDSupra

- Federal Register :: Request Access

- PDF (https://www.sec.gov/files/regulation-crowdfunding-2019_0.pdf)

- PDF (https://www.crowdfundinsider.com/wp-content/uploads/2020/09/Regulation-Crowdf...)