SME Lending Software Overview

No time to read? Let AI give you a quick summary of this article.

Small and medium-sized enterprises (SMEs) are the foundation of economies worldwide1. They drive innovation, ensure employment and boost economic growth. Access to finance is crucial for these businesses to start, operate, and expand. However, obtaining necessary funding has been a persistent challenge for many SMEs.

This article explores SME lending, the types of projects involved, the opportunities and challenges businesses face, and provides an overview of key SME lending software solutions that are transforming the landscape.

What you will learn in this post:

Understanding SME lending

SME lending refers to the provision of financial services, primarily loans, to small and medium-sized enterprises. These loans can be used for various purposes2, including:

- real estate

- new venture financing

- working capital

- equipment purchases

- expansion projects, etc.

Types of SME lending projects

Let’s take a closer look at various goals and types of SME lending.

Real estate financing

Many SMEs invest in real estate to establish offices, manufacturing units, or retail spaces. Small developers or construction firms build or renovate residential properties, such as apartments or housing complexes, for sale or rental. Such projects require significant financing and may come with longer repayment terms.

Startup lending

Newly established businesses require funding to develop products or services, conduct market research, and cover initial operational costs. Startups typically look for investments from angel investors, venture capital firms, or they opt for small business loans.

Financing equipment purchases

SMEs often need to purchase machinery or technology to enhance productivity. Equipment loans or leases are common financing methods for these needs.

Loans for getting working capital

To manage daily operations, SMEs may require short-term loans to cover expenses like payroll, inventory, and utilities.

Expansion projects

Businesses that are planning to grow may need to enter new markets, launch new products, or acquire other businesses.

Opportunities and challenges in SME lending

SME lending presents compelling opportunities for investors, but not without challenges. Let’s talk about the opportunities first.

High yield potential

SME loans typically offer higher returns compared to traditional fixed-income investments. Interest rates on SME loans vary depending on the risk profile of the borrower, but they often exceed the rates of corporate bonds and government securities. For example, marketplace lending platforms report annual returns ranging from 5% to 15%3, which is significantly higher than many conventional investment options.

Portfolio diversification

Investing in SME loans allows investors to diversify their portfolios4 across industries, geographic locations, and loan types. Unlike stock market investments, which can be volatile and correlated with economic cycles, SME lending provides an alternative asset class with lower correlation to traditional financial markets. By spreading investments across multiple businesses, investors can mitigate risks and enhance portfolio stability.

Direct access to alternative finance markets

Investors can now participate in loans through alternative finance platforms,such as peer-to-peer lending and crowdfunding platforms without the need for intermediaries. These platforms offer transparency, real-time analytics, and risk assessment tools that enable investors to make informed decisions.

Impact investing and economic growth

Investing in SME lending is not only about financial returns. By providing capital to growing businesses, investors support entrepreneurship and contribute to financial inclusion. Many investors now prioritize ESG (Environmental, Social, and Governance) criteria5, and SME lending aligns with these principles by supporting small businesses that promote sustainability and social impact.

Access to investment opportunities for retail investors

Retail investors, on the other hand, can participate through crowdfunding platforms with relatively low minimum investment requirements, as many platforms allow to invest as low as $100 per loan.

Risks and challenges of SME lending

While SME lending offers attractive returns and diversification benefits, it also carries specific risks that investors must understand and know how to mitigate.

Default risk

Investing in SMEs generally poses a higher credit risk than investing in established corporations due to their smaller financial reserves, limited credit history, and higher vulnerability to economic fluctuations. Many small businesses operate with thin profit margins and may struggle to meet debt obligations during economic downturns or unexpected financial disruptions.

To mitigate this risk, it is recommended to spread investments across multiple SMEs. Some SME lending platforms offer secured loans by assets such as real estate, equipment, or accounts receivable. This reduces potential losses in case of default.

Liquidity concerns: Limited markets for reselling loans

Unlike stocks or bonds, SME loans are not typically traded on public markets. This makes them relatively illiquid. Once an investor commits capital to a loan, withdrawing it before maturity can be challenging. This lack of liquidity means investors may need to wait months or even years to see returns, depending on loan repayment schedules.

To mitigate this risk, it is recommended to invest in short-term loans. Some SME lending platforms offer short-term loans with repayment within 3-12 months6 rather than multi-year commitments. A few lending platforms provide secondary markets where investors can sell their loan shares to other investors, though demand can vary. Investors can also combine SME lending with more liquid assets such as publicly traded stocks or bonds,

Regulatory challenges

The SME lending industry is subject to evolving regulations that vary by country and financial jurisdiction. Governments often impose strict compliance requirements on lending practices to protect borrowers and ensure financial stability. These regulations can impact investor returns by imposing additional costs, limiting lending terms, or restricting access to certain markets.

Investors participating in lending platforms may need to comply with local financial regulations, which can be complex.

To navigate regulatory challenges, investors should stay updated on regulatory changes in the regions where they invest and work only with well-established regulated lending platforms.

The role of SME lending software

To address the risks, challenges, streamline customer onboarding and lending processes, companies that provide SME lending services use SME lending software.

Software is used to enhance efficiency, reduce costs, and improve risk assessment in SME lending. Below is an overview of some SME lending software solutions worldwide.

LenderKit

LenderKit is a white-label crowdfunding and investment management software designed to provide businesses with comprehensive control over their online investment operations.

The platform caters to various use cases including real estate, private equity, equity crowdfunding, SME lending and impact investing.

It offers a customizable back-office system that allows to manage investors and borrowers, monitor offerings and payment statuses, and generate detailed reports and analytics.

LenderKit’s pricing comprises several components:

- License costs include subscription fees which can be monthly, quarterly, or yearly.

- Service costs related to design or functionality customizations, quality assurance, business analysis, project management and consulting.

- Post-launch support & maintenance are optional services available after the project’s release.

For detailed pricing information, potential clients are advised to contact LenderKit directly, as costs vary based on the level of customization and specific project requirements.

HES Fintech

HES Fintech7 offers a white-label lending platform that automates loan origination and management processes. The platform includes modules for customer onboarding, KYC/AML compliance, scoring, and loan servicing. It is customizable and can be implemented within a few months, offering GDPR and ISO compliance.

Loandisk

Loandisk8 is an online loan management system designed for microfinance companies, credit unions, and small lenders. It offers features such as client management, loan tracking, payment scheduling, and reporting. The platform is cloud-based which ensures accessibility and data security.

Loandisk offers six distinct pricing plans, each with a 30-day free trial.

All plans include features such as unlimited branches, borrowers/clients, repayments, staff roles and permissions, borrower login, email and SMS capabilities.

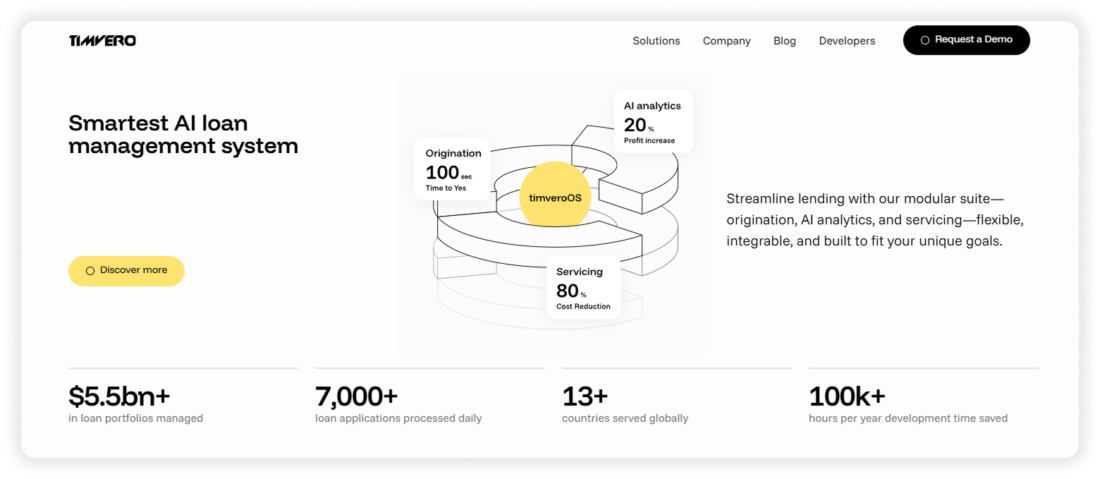

Timvero

Timvero9 offers a comprehensive loan management system powered by artificial intelligence. The platform includes modules for loan origination, advanced analytics, and loan servicing. It is designed to be flexible and integrable, catering to the unique goals of various lending institutions. Timvero’s AI capabilities enable smart data processing, enhance decision-making and operational efficiency.

Provenir

Provenir10 provides an AI-powered risk decisioning platform that supports fintech companies in making faster and more accurate lending decisions. The platform enables seamless financial experiences and hyper-personalization and helps lenders to grow their market share. Provenir’s scalable and flexible platform is designed to support businesses from startup to large enterprises.

Conclusion

Selecting the appropriate lending software is crucial for SMEs aiming to optimize their lending operations.

At LenderKit, we provide white-label debt crowdfunding software to help you launch your P2P lending platform or an investment marketplace.

Combined with useful integrations for payment processing, KYC/AML compliance and digital document management, our software provides robust out-of-box functionality, but can also be fully customized to fit your business needs and regulatory requirements.

If you’d like to discuss further, don’t hesitate to contact us.

Article sources:

- World Bank SME Finance

- Blog – Capital Bank

- An investor’s guide to marketplace lending | U.S. Bank

- Validus Group - Homepage

- Investors now prioritize ESG (Environmental, Social, and Governance) criteria

- Get Funded in 90 Seconds – Short-Term Business Loans for UK SMEs

- Loan Management & Lending Automation Software

- Loandisk - Online Loan Management System for Microfinance Cos

- TimveroOS — Framework-Native Lending OS & SDK

- Shaping the Future of Decisioning with AI - Provenir