Crowdlending For Businesses: The Ultimate Guide

No time to read? Let AI give you a quick summary of this article.

Access to capital has always been one of the biggest challenges for businesses. Traditional bank loans are often slow, rigid, and difficult to secure, especially for small and medium-sized companies. Over the past decade, a different model has gained traction across Europe, particularly in Germany, the Netherlands, and Spain: crowdlending.

This guide touches everything from crowdlending definition to how it works in practice, what types of crowdlending exist, and how businesses can use leading crowdlending platforms and crowdlending software to access funding.

What you will learn in this post:

What is crowdlending?

Crowdlending is a way for businesses to borrow money from a large number of individual investors via online platforms instead of relying on a single bank or financial institution.

It is often referred to as P2P crowdlending (peer-to-peer lending), although in practice, modern platforms are far more than simple intermediaries. They structure loans, assess borrower risk, set terms, and manage repayments on behalf of investors.

Unlike traditional crowdfunding, crowdlending is strictly debt-based:

- The business is legally obligated to repay the loan

- Investors earn a fixed or variable interest return

- Loan terms (amount, duration, rate) are defined upfront

From a regulatory standpoint, crowdlending has evolved quickly over the past decade, particularly in Europe, where the model is most widely used.

In the European Union, platforms operate under the European Crowdfunding Service Providers Regulation. This framework created a single licensing system across member states and applies to platforms offering business loans of up to €5 million.

It also introduced clear rules in several key areas:

- Investor protection, including risk disclosures and basic knowledge checks

- Transparency around fees, risks, and loan terms

- Mandatory authorization and supervision by national regulators

- Standardized investment information for every listed opportunity

In practice, this means platforms must be licensed or registered and comply with strict requirements such as anti-money laundering (AML) checks and investor protection standards.

Outside the EU, the approach is less uniform. In the United Kingdom, platforms are regulated by the Financial Conduct Authority1. In the United States, regulation is stricter and more fragmented, with platforms operating under securities laws enforced by the Securities and Exchange Commission2.

Overall, regulation has made crowdlending more structured and transparent. At the same time, it has raised the bar for both platforms and participants. Businesses need to factor this in when choosing where and how to raise capital.

In practical terms, crowdlending now sits between traditional bank loans and capital markets: easier to access than bank financing, but regulated enough to provide a level of trust and stability.

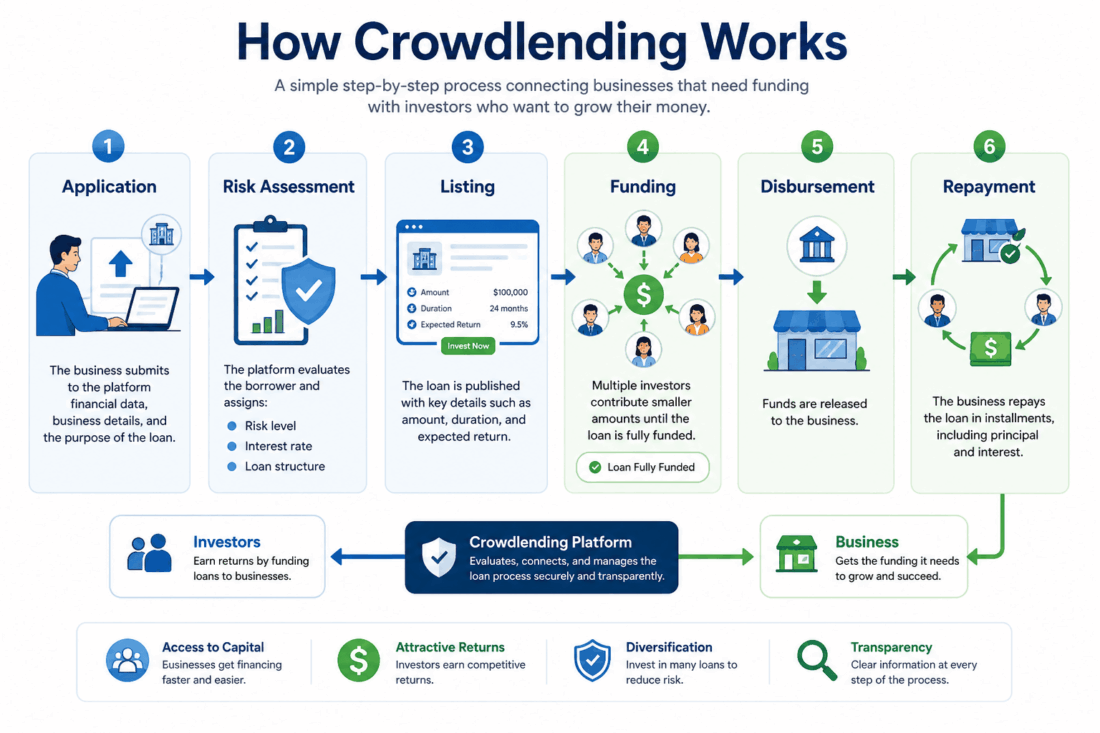

How crowdlending works

Despite the name, crowdlending is not informal. It follows a structured process.

1. Application

The business submits to the platform financial data, business details, and the purpose of the loan.

2. Risk assessment

The platform evaluates the borrower and assigns:

- Risk level

- Interest rate

- Loan structure

3. Listing

The loan is published with key details such as amount, duration, and expected return.

4. Funding

Multiple investors contribute smaller amounts until the loan is fully funded.

5. Disbursement

Funds are released to the business.

6. Repayment

The business repays the loan in installments, including principal and interest.

Why businesses use crowdlending

Crowdlending has gained traction because traditional financing does not serve every type of business equally well. Banks tend to favor established companies with long track records, strong collateral, and predictable cash flows. That leaves a gap, especially for small and medium-sized businesses, newer ventures, and projects that don’t fit standard credit models.

Crowdlending offers a more accessible and flexible route to capital.

Along with it, there are some more advantages that businesses get from crowdlending.

More flexible requirements

Traditional lenders often require significant collateral, strict financial ratios, and extensive credit history. Crowdlending platforms tend to be more loyal3. While risk assessment is still part of the process, businesses may qualify based on project viability, revenue potential, or asset backing (especially in crowdlending real estate), rather than purely on past financials.

Diversified funding sources

Instead of relying on a single bank or lender, businesses raise capital from many individual investors. This spreads risk and reduces dependency on one financing partner. It also creates more stability, because if one source pulls back, the entire funding structure doesn’t collapse.

Market validation through investor demand

Crowdlending does more than provide capital; it tests demand. If a project attracts funding quickly, it signals confidence from the market. If it struggles, that can be an early warning sign. In that sense, crowdlending acts as both a financing tool and a feedback mechanism.

Greater control over terms and positioning

Many platforms allow businesses to define key parameters such as loan amount, duration, and sometimes even pricing within certain ranges. While not completely unrestricted, this is often more flexible than bank lending, where terms are largely dictated by the institution.

Crowdlending is not always cheaper than a bank loan. Interest rates can be higher, especially for riskier projects or borrowers without a strong track record. In addition, platforms may charge listing or servicing fees, which need to be factored into the total cost of capital.

However, cost is only one part of the equation. For many businesses, the real advantage is access. If bank financing is slow, restrictive, or simply unavailable, crowdlending becomes a practical alternative.

Types of crowdlending

Crowdlending is not a single model. It includes several variations.

Business crowdlending

Business crowdlending is the most relevant model for companies. Funds raised through business crowdlending are typically used for operational or growth-related needs, such as:

- Expanding into new markets or locations

- Hiring staff and scaling operations

- Covering working capital gaps (inventory, payroll, short-term liquidity)

- Investing in equipment or infrastructure

This type of financing is especially useful for small and medium-sized enterprises that may not meet traditional bank lending criteria but have stable revenue or clear growth potential. It also allows businesses to raise funds without giving up equity, which is a key distinction from venture capital.

Consumer crowdlending

Consumer crowdlending focuses on loans issued to private individuals rather than businesses. While it is a major segment in the broader peer-to-peer lending ecosystem, it is less relevant for corporate finance.

In this model, individuals borrow money for personal use, such as debt consolidation, home improvements, or large purchases, and repay it with interest through structured installments.

For businesses, this category is mainly irrelevant.

Property crowdlending

Crowdlending real estate4 is one of the fastest-growing and most established segments within the industry. It focuses specifically on property-related financing and has become a preferred option for both developers and investors.

In this model, capital raised from investors is used for real estate projects such as:

- Property development and construction

- Renovation or redevelopment of existing buildings

- Bridge financing between acquisition and long-term refinancing

- Short-term liquidity for real estate transactions

What makes this segment particularly attractive is the presence of tangible collateral. In many cases, loans are secured against the property itself, which reduces perceived risk for investors compared to unsecured lending.

This structure has made real estate one of the most active areas5 in crowdlending platforms, especially in European markets like Spain, Germany, and Netherlands6, where property investment culture is strong and regulated platforms are widely used.

For businesses in the real estate sector, crowdlending offers a practical alternative to traditional bank mortgages, particularly for time-sensitive deals or projects that require flexible financing structures.

Top 5 crowdlending platforms: How they actually work

Not all crowdlending platforms operate in the same way. The structure behind each platform determines how loans are issued, where the risk sits, and how suitable it is for different use cases.

Here are the top crowdlending platforms that focus on different niches7.

Mintos

Mintos8 is one of the largest crowdlending marketplaces in Europe, but it does not originate loans itself. Instead, it acts as an aggregator that connects investors with loans issued by external lending companies. These lenders upload their loan portfolios to the platform, and investors fund them indirectly.

This model creates strong diversification. A single investment can be spread across different countries, loan types, and borrower profiles. At the same time, it introduces an additional layer of risk. Investors are exposed not only to borrowers but also to the lending companies behind the loans.

Mintos operates on a relatively transparent fee structure, but costs depend on how the investor uses the platform:

- Investor fees: Typically 0% platform fee for standard investing activities

- Secondary market fee: Around 0.85% of the sale price when selling loans early on the marketplace

- Currency conversion fees: Apply when investing in loans denominated in currencies different from the investor’s account currency

On the lender side, loan originators pay listing and servicing fees to Mintos, which are not directly charged to investors but indirectly reflected in loan pricing and yields.

Expected returns have historically ranged from 5% to 12% annually, depending on loan type, risk level, and economic conditions.

EstateGuru

EstateGuru4 focuses exclusively on crowdlending real estate, which sets it apart from general platforms. Every loan is tied to a property project and backed by real estate collateral, typically involving development or renovation.

Borrowers are usually property developers who are looking for short- to medium-term financing. For investors, this makes the model easier to understand because each loan is linked to a tangible asset.

Minimum investments are typically low, often starting around €50 per investment. Targeted annual returns usually range between 8% and 12%, depending on project risk and location.

However, this structure comes with trade-offs. Liquidity is lower, loan durations are longer (6 to 36 months), and performance depends on real estate market conditions. EstateGuru is more structured and asset-driven, but less flexible compared to general marketplaces.

Funding Circle

Funding Circle9 is one of the best-known crowdlending platforms focused specifically on small and medium-sized business loans. Unlike marketplace aggregators, it operates more as a direct lending platform. It connects investors with loans issued to established businesses seeking financing for growth and operations.

The platform specializes in SME credit, meaning loans are typically used for working capital, expansion, hiring, or refinancing existing debt. Borrowers are usually small and medium-sized companies with an established trading history. This makes the risk profile more structured compared to consumer-only lending platforms.

This model creates a more direct exposure to business lending. Investors are not diversifying across multiple third-party originators, but instead participating in a pool of business loans assessed and managed by Funding Circle itself.

Funding Circle does not typically charge investors direct platform fees for standard investing activity. Secondary market fees may apply when selling loans early. These fees depend on the market and the product.

Historically, expected returns on SME loans have typically ranged between 4% and 8% annually. However, returns are closely tied to economic cycles. During downturns, small businesses are more sensitive to cash flow disruptions, which can increase default risk.

PeerBerry

PeerBerry10 operates as a marketplace, but with a more controlled structure than larger platforms like Mintos. It works with a smaller group of lending partners, most of which belong to the same lending ecosystem.

Loans are typically short-term and relatively standardized. This creates a more stable and predictable environment, with consistent returns over time.

Minimum investment is typically around €10 per loan fraction. Average loan terms usually range from 30 to 90 days. Expected returns are generally in the range of 7% to 12% annually.

However, the trade-off is reduced diversification. Because the platform relies on fewer lenders, risk is more concentrated. PeerBerry is easier to manage and more predictable, but less flexible and less diversified.

LendingClub

LendingClub11 is one of the most established peer-to-peer crowdlending platforms in the United States. Unlike European marketplace models, LendingClub operates as a regulated financial institution that originates loans directly and funds them through its investor base, rather than acting purely as a connector between third-party lenders and investors.

The platform focuses primarily on consumer and small business loans. This structure creates a more centralized and regulated environment compared to open marketplaces like Mintos or PeerBerry. Risk assessment is standardized, but diversification depends heavily on investor allocation strategies rather than access to multiple external loan originators.

The minimum investment is typically $1 per loan fraction, making entry highly accessible. The average returns are around 4% to 8% annually, depending on risk grade and economic conditions. The loan duration varies from 36 to 60 months for personal loans, and shorter for business credit lines.

Crowdlending software: The infrastructure behind it

Behind every platform sits a layer of crowdlending software that makes the entire system work. Different software providers cater to different platforms and needs.

HES FinTech

HES FinTech12 is a lending software provider focused on end-to-end loan management systems for banks, fintech companies, and alternative lenders. It offers tools like loan origination, credit scoring, underwriting automation, and servicing workflows.

HES FinTech pricing is not publicly fixed. Costs are customized based on scope, modules, and deployment needs.

Typical pricing range:

- Starting cost: from ~$75,000+ per year / project

- Setup fee: one-time implementation cost (varies significantly)

- Ongoing licensing: depends on usage and selected modules

- Customization costs: additional budget for integrations and advanced features

In short, pricing is negotiated case by case and aimed at banks and large fintech lenders, not startups or lightweight platforms.

LendFoundry

LendFoundry13 is a modular lending infrastructure platform built for large-scale financial institutions. It uses a microservices architecture that allows companies to build custom lending systems via APIs.

It is highly flexible but also highly technical, requiring strong development resources to implement.

LendFoundry is an enterprise lending infrastructure platform with custom, non-public pricing.

Pricing varies:

- Starting cost: custom, depends on integrations and usage

- Implementation: significant one-time setup and integration costs

- Ongoing costs: depend on API usage, modules, and infrastructure scale

Overall, pricing is negotiated individually and aimed at large financial institutions building custom lending systems via APIs.

LenderKit

LenderKit is a white-label crowdfunding and investment platform builder designed for companies that want to launch their own crowdlending, P2P lending, or real estate investment platforms without building infrastructure from scratch. It provides ready-made modules for investor onboarding, deal management, portfolio tracking, payments, and platform administration.

Unlike backend-only lending systems or compliance tools, LenderKit is focused on the full end-to-end experience of running an investment marketplace, including both the investor and borrower sides.

LenderKit doesn’t share pricing publicly, but the company provides software on subscription. The services also include custom crowdfunding platform development and customizations of the existing solution.

LenderKit software is suitable for both startups and established businesses, such as fintechs and investment companies, that want to launch a platform quickly without building core infrastructure internally.

Looking for a ready-made solution or exloring a custom build?

Here's how we can help

Why LenderKit is the best option for launching a crowdlending platform

LenderKit stands out because it is the only solution in this group that is purpose-built for launching investor-facing crowdlending platforms, rather than supporting only one part of the ecosystem.

Compared to other providers:

- HES FinTech focuses on internal lending operations, not investor marketplaces

- LendFoundry provides infrastructure APIs, but requires heavy engineering and long development cycles

LenderKit combines what these tools separate:

- Ready-made crowdfunding marketplace

- Investor and borrower management tools

- Loan and deal lifecycle workflows

- Regulatory-ready structure for multiple jurisdictions

- Faster time-to-market without building from scratch

This makes it particularly suitable for companies in countries where regulated crowdlending markets require both compliance and a fully functional investment platform from day one.In practice, LenderKit is the most direct path for teams that want to launch, operate, and scale a crowdlending platform as a business. To discuss details or see how the product works, please get in touch with our team.

Article sources:

- Financial Conduct Authority | FCA

- SEC.gov | Home

- Peer-to-peer lending - Wikipedia

- Invest in Property Loans for a Steady Monthly Income

- ESMA: Crowdfunding in the EU

- Securities Crowdfunding: There Are Over 230 ECSPR Platforms Operating In Europe | Crowdfund Insider

- Exploring 10 Niches Revolutionized by Crowdfunding

- Home Page

- Fast, Affordable Small Business Finance

- Alternative investment platform - PeerBerry

- Online Personal Loans + Online Banking | LendingClub

- Loan Management Software & Lending Automation | HES FinTech

- Cloud-Based Best Alternative Lending Software | Digital Lending Platform